Wall Street and Silicon Valley have poured billions of dollars into electric vehicle and related companies in 2020, betting on their future dominance and in many cases fueling valuations that have little to do with the companies’ current or expected production and sales.

There is little doubt that the automotive industry is trending toward electric vehicles amid the rise of Tesla Inc. TSLA,

Falling prices and increasing availability of electric vehicles, or cars; the potential for technological breakthroughs that offer a cheaper, longer and longer rechargeable battery; advances in EV infrastructure, and ‘green-friendly’ government initiatives taking root in the US and elsewhere point the way.

And what was once an investment universe consisting only of Tesla and a few fuel cell companies, has grown into a sub-sector that combines industry, technology and transportation, with China as a key driver, as well as the basic market for the EV manufacturer than for the demand for EV. In total, at least $ 28 billion has been invested in public and private electric vehicle businesses by 2020, according to data from CB Insights and Dow Jones Market Data Group.

Do not miss: the explosion in the financing of electric vehicles, valuation and trading in one graph

“The writing is on the wall regarding the long-term debate against internal combustion,” said John Mitchell, a partner at Blue Horizon Capital.

In several countries around the world, people will no longer be able to buy internal combustion engines in a short decade or two, and global car manufacturers have realized that ‘the transition to electric vehicles is the only way to compete’, he said. .

It should not be surpassed, General Motors Co. GM,

Ford Motor Co F,

and other old-fashioned automakers have increased investments in motor vehicles and autonomous vehicles, with GM promising to phase out vehicles with internal combustion engines in less than 15 years. Tesla, of course, joined the S&P 500 index SPX,

in 2020 after finally showing steady gains. SPX,

New companies like Nio Inc. NIO,

Nikola Corp NKLA,

and Fisker Inc. FSR,

attracted the attention of large investors, and the involvement of companies for special acquisitions has become almost a common place.

“The EV party has just started tightening its seat belts,” Wedbush analyst Dan Ives said recently. Recent weakness is short-term ‘growth pains’, he said.

This does not mean that the transition from internal combustion engines to electric motors will take place quickly. Electric cars currently account for about 2% of global car sales, and estimates for a future market share range from a low forecast of 10% to 20% of cars sold by 2030 to as much as two-thirds of the market. time.

Much more money will be needed to finance the switch, despite the billions that have already found their way to EV-related investments. A recent note from B. of A. Securities placed a price tag on a future EV ‘revolution’ and said that financing the change is still a ‘huge obstacle’.

The B. van A. analysts calculate that a move to a 100% EV world will require more than $ 2.5 trillion in investments, coming from companies, investors and governments across the economy between Tesla’s capital increases and the ability to drive vehicles to manufacture. the world.

Recent capital increases by EVs and related companies through the SPACs, or ‘blank-check’ companies, ‘may just be a start’, they said.

‘Hyper growth’ in EV and renewable energy

The increased interest in EV and related stocks has raised concerns about a bubble.

At a recent JPMorgan virtual investor conference, Joyce Chang and other research leaders told the audience that they do not see a “broad stock market bubble” but that “certain pockets” of the market are experiencing “hyper-growth, such as electricity.” vehicles and renewable energy. ”

Bubbles are of course easy to spot – seen afterwards. It remains to be seen whether the current inflow of money and attention to EV companies, as well as autonomous vehicles and AV-related companies, will look like the short-lived notice paid to cloud computing companies half a decade ago, or the early spotlight on fuel cell companies, several of which – 20 years later – still have not returned to the record highs established at the time.

The Tesla bubble: Bets on electric cars and the rise of SPACs have led to a new version of the dot-com boom, writes columnist Therese Poletti

JPMorgan analysts reminded the audience that EVs, renewable energy sources and ‘innovation’ stocks make up a small percentage of the broader stock market, with EVs accounting for only about 2% of the S&P 500.

However, Blue Horizon’s Mitchell is good for the future and points to the increasing quality and technical improvements for EVs.

“The battery life will only be extended and with the trillions invested worldwide by everyone who supports the electrification of the transport system, the infrastructure for the widespread use and use of EV technology will only increase,” he said.

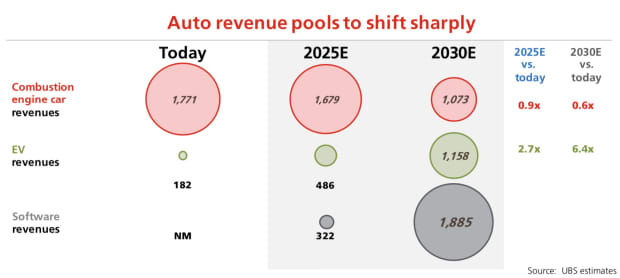

UBS analysts predict that carmaker revenues worldwide will move to $ 1.16 trillion by the year 2030, from $ 182 billion today.

Conversely, revenue from ICE vehicles will drop from $ 1.77 trillion today to $ 1.07 trillion. Revenue for software will form a larger share of revenue by 2030, at almost $ 2 billion.

Here is the UBS chart, in billions:

A company or a business plan?

Blank check companies have been around for a long time, but took over a larger role in U.S. investment last year, when there were more initial public offerings by specialty procurement companies than all other years combined, Garrett Nelson told CFRA said. recent note.

The activities in 2021 are on track to exceed ‘by a wide margin’ last year, and some of the largest SPAC transactions are likely to be in the ’emerging electric and autonomous vehicle (EV / AV) space’ again, he said.

Some of the businesses that do look like business plans rather than revenue or profit-generating businesses, but there is reason for optimism, Nelson said.

The CFRA analyst has singled out Fisker, Lucid Motors, who plans to merge with Churchill Capital Corp. via a SPAC merger. IV CCIV,

and the private manufacturer of electric trucks, Rivian, as companies that are better positioned than others.

Tesla, of course, has established a lead advantage that is widely considered substantial.

UBS analysts calculate that Tesla has a cost advantage of about $ 1,000 to $ 2,000 per electric vehicle over other automakers, although competition is increasing. Volkswagen AG’s VOW,

MEB platform, the car block for its electric vehicles, is already ‘fully cost-effective’ with Tesla.

VW, the no. 2-car manufacturer in the world, still lags behind in terms of battery costs, with Tesla likely to retain its price advantage in the battery due to its vertical integration and technological advancement. Yet they see that big old-fashioned manufacturers like VW could achieve an EV manufacturing cost and margin parity within four years.

EVs, not AVs, can be the right game changer

Related to the influx of investors to electric vehicle manufacturers is holding the interest by lidar, batteries, sensors and other components that are the key to autonomous vehicles.

Full autonomy has been proven to be a stubborn and costly problem to solve, with many regulatory and technological barriers.

Despite high goals, most cars on the road today offer advanced driver assistance systems that do not differ dramatically from previous years’ systems, and are far from the game changer they are expected to be for life and economically. distant future.

For now, automakers are mostly focusing on partial autonomy and ADAS offerings that can be commercialized in the short term, with EVs continuing in terms of consumer interest and regulatory pressure.

“EVs are simply a better product,” Blue Horizon’s Mitchell said.